Short view on Innovative Solutions and Support

Activities, Financial data and potential Price Target

Short view :

Company : Innovative Solutions and Support, Inc. (ISSC)

Ticker : ISSC

Market cap : $103.87M

Revenue : $53.9 million LTM

Adj EBITDA : $13.3 million LTM (25% EBITDA margin)

EV/Sales : 2x ntm

EV/EBITDA : 6.6x ntm

1. History

Innovative Solutions and Support, Inc. (ISSC) was founded on February 12, 1988, by Geoffrey S. M. Hedrick and is headquartered in Exton, Pennsylvania. The company began as a systems integrator focused on designing and manufacturing advanced avionics solutions, particularly for retrofit applications and original equipment manufacturers (OEMs). ISSC went public on August 4, 2000, with an initial stock price of $8.13. Over the years, it has evolved into a key player in the aerospace and defense industry, specializing in flight guidance, autothrottle, and cockpit display systems. Notable milestones include the acquisition of a license for Honeywell’s Display Generator and Flight Control Computer product line, strengthening its position in the military market, and the integration of its ThrustSense® Autothrottle into the U.S. Army C-12 fleet.

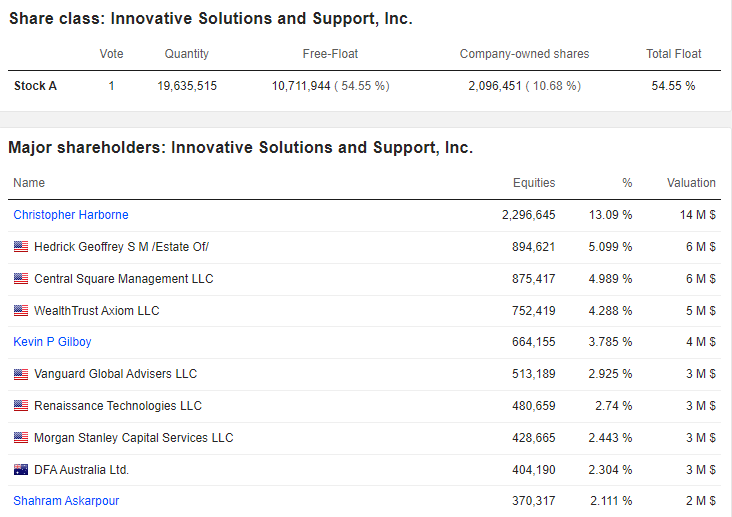

2. Ownership

ISSC is a publicly traded company listed on the NASDAQ under the ticker symbol ISSC. As of March 2025, the company has 17,584,037 outstanding shares. The ownership structure includes a mix of institutional, insider, and retail investors:

We can see that the number 1 shareholder, Harbonne, recently sold on top at $11. He had launched a takeover bid for $7.5, which was rejected by the board. Nevertheless, he remains the number 1 shareholder.

3. Activities

ISSC designs, develops, manufactures, sells, and services advanced avionic solutions for commercial, business, aviation, and military markets. Its product portfolio is categorized into five key areas:

Integrated Flight Deck Systems (COCKPIT/IP): Includes crew alerting systems, engine displays, integrated standby instruments, and mission displays.

Navigation Systems: Offers flat panel display systems, global positioning system (GPS) receivers, and flight management systems that replicate analog or digital displays for legacy aircraft upgrades.

Communication Systems: Provides communication and navigation products, including LPV navigators and inertial reference systems.

Sensors and Control Systems: Includes air data products and utilities management systems.

Advanced Flight Actuators: Features the ThrustSense® Autothrottle, which automates engine power settings to reduce pilot workload and enhance safety.

The company serves both retrofit applications (upgrading existing aircraft) and OEMs, with a focus on reducing carbon footprints through efficient navigation systems. ISSC’s products are used in commercial air transport, corporate/general aviation, military aircraft, and security monitoring on-board aircraft.

4. Strategy

ISSC’s strategic initiatives are centered on growth, innovation, and market diversification:

Acquisitions and Partnerships: The acquisition of Honeywell’s product line has expanded ISSC’s military market presence. Strategic acquisitions are expected to enhance revenue through diversification and integration of technologies like AI.

Product Innovation: ISSC is investing in AI-enabled autonomous flight systems and advanced avionics to maintain a competitive edge. The IS&S Next strategy focuses on next-generation technologies to improve operating margins.

Manufacturing Expansion: The company is expanding its manufacturing capabilities to support increased production, particularly for military programs.

Military Market Focus: ISSC is leveraging contracts like the U.S. Army C-12 fleet deal to strengthen its position in the defense sector.

Cost Efficiency and Margin Improvement: By optimizing production and integrating acquired technologies, ISSC aims to boost profitability.

5. Clients and Suppliers

Clients: ISSC serves a diverse customer base, including:

Commercial air transport carriers.

Corporate and general aviation companies.

The U.S. Department of Defense (DoD) and its commercial contractors.

Aircraft operators, modification centers, government agencies, and foreign militaries.

OEMs such as airframe manufacturers.

Specific contracts include the U.S. Army for the C-12 fleet and partnerships with military contractors.

Suppliers: While specific supplier details are not publicly disclosed, ISSC relies on a supply chain for components like sensors, displays, and software. The acquisition of Honeywell’s product line suggests a strategic supplier relationship with Honeywell, providing access to proprietary technology and components.

6. Financial Data

ISSC has solid fundamentals. With the acquisition of part of Honeywell's operations, the annualized revenue growth rate is 24.4% over the past five years. EBITDA margins are improving. This is explained by several factors:

— Diverse product portfolio

— Strengthening relationships and penetration within OEM accounts

— Ability to win against competitors

— Expanding through new product introductions

The strong improvement in EBITDA and net income is driven by:

— Ability to pass through raw material cost increases

— Increased capacity utilization, resulting in greater absorption of operating costs through cost of goods sold (COGS)

— Operating leverage created through sales growth

— Process efficiencies achieved

— Favorable product mix

The company has low leverage at 2x EBITDA. Debt has increased to finance the acquisition of Honeywell's operations.

7. Perspectives and Outlook

Growth Drivers:

Military Contracts: The U.S. Army C-12 deal and Honeywell integration are expected to drive revenue in the second half of 2025.

AI and Autonomy: Investments in AI-enabled flight systems position ISSC to capture emerging opportunities in autonomous aviation.

Manufacturing Expansion: Increased capacity supports higher production volumes, particularly for defense programs.

Strategic Acquisitions: Further acquisitions could diversify revenue streams and enhance technological capabilities.

Risks and Challenges:

Honeywell Transition Delays: Delays in integrating Honeywell’s product line could impact financial performance.

U.S. Defense Budget Cuts: Potential reductions in defense spending may affect military contracts.

Tariff Policies: Trade uncertainties could disrupt supply chains or increase costs.

Analyst Sentiment: Four analysts cover ISSC. Analysts are forecasting strong growth in the coming years, with revenues expected to reach $72.16M in FY 2026 (16.39% growth) and $87.95M in FY 2027 (21.88% growth). This growth is primarily driven by the markets the company serves, thanks to recent acquisitions and the continuity of its operations. Earnings per share (EPS) are also accelerating significantly due to the revenue growth effect and improving margins.

This results in a low valuation by 2027

If we apply a valuation of 17x EPS, the share price in 2027 could reach $14.

If we use a valuation of 2.2x sales, we get a price of $11 in 2027.

8. What to Think of This Company?

ISSC is a company with expertise and high-value-added technologies in a sector critical to the USA—avionics and defense. It presents compelling drivers for achieving a strong return on investment (ROI) with a price target near $11:

Potential for a Takeover (OPA): There’s speculation about a possible return of Harbonne or another strategic buyer, which could drive the stock price higher.

Strong Financial Growth: As highlighted in the financial data, ISSC has shown robust revenue growth (24.4% annualized over five years) and improving EPS, with projections of $72.16M in revenue for FY 2026 and $87.95M in FY 2027. The EPS is expected to reach $0.83 by FY 2027, supported by margin improvements and operational efficiencies.

Strategic Acquisitions: The Honeywell acquisition has already bolstered ISSC’s military market presence, and further strategic acquisitions could enhance revenue diversification and technological capabilities.

However, there are areas of caution to monitor:

Margin Sustainability Post-Acquisitions: The integration of Honeywell’s operations has driven growth, but delays or inefficiencies could pressure margins, especially if raw material costs rise faster than anticipated.

Industrial Risks: Manufacturing expansion and reliance on a complex supply chain expose ISSC to risks like production delays, quality issues, or supply chain disruptions.

Turbulence in the U.S. Defense Sector: Potential defense budget cuts, policy shifts, or geopolitical uncertainties could impact ISSC’s military contracts, which are a significant revenue driver.

Conclusion

ISSC is a promising investment with strong fundamentals, high growth potential, and an attractive valuation (current price of $6.6 versus a fair price estimate between $11–$14). Its position in a critical sector, combined with acquisition-driven growth and technological innovation, makes it a candidate for solid returns. However, investors should remain vigilant about integration risks, margin pressures, and broader defense sector challenges. Balancing these factors, ISSC appears to offer a favorable risk-reward profile, particularly for those optimistic about its takeover potential and long-term growth trajectory.

I am currently a shareholder of the company. These posts are not a recommendation to buy. You must do your own research.